Risk¶

In general, the vast majority of us dislike risk.

Imagine we offer you two retirement plan:

Plan A: sure income of: 50 000/an

Plan B: An uncertain retirement plan (say because it depends on returns)

Plan B

50% chance 10 000/yr

50% chance 90 000/yr

Even if the expected income is 50 000 in both cases, you are very likely to prefer Plan A…

Risk and Return¶

Imagine we modify Plan B to get:

Plan C

50% chance 20 000/yr

50% chance 90 000/yr

or even Plan D,

Plan D

50% chance 40 000/yr

50% chance 90 000/yr

Expected income is now higher than with plan A. If we keep increasing the downside, you will at some point prefer the risky plan. Hence, preferences in risky situations are not only function of the expected gain but also risk (probabilities and payoffs). As of now, our theory does not cover these cases.

Expected Utility (EU)¶

Lotteries

Consider a payout \(Z\). There is a lottery \(L = (p,X \;; 1-p,Y)\) : with probability \(p\) of getting \(Z=X\), and probability \(1-p\) of getting \(Z=Y\).

The expected wealth from the lottery is \(\mathbb{E}_{L}Z = pX + (1-p)Y\).

To represent preferences, taking the expectation of utility is intuitively appealing:

\[\mathbb{E}_{L} u = p\times u(X) + (1-p) \times u(Y)\]

Preferences over Lotteries

The consumer prefers the lottery \(L_1\) to lottery \(L_2\) if

\[\mathbb{E}_{L_1} u > \mathbb{E}_{L_2} u\]

The representation of preferences by expected utility is due to von Neumann et Morgenstern often abbreviated vNM preferences.

This formulation imposes several testable restrictions on choices. We will come back to this later.

Example

If \(u(Z) = \sqrt{Z}\) and the consumer faces lotteries \(\mathcal L_1 = (0.5,0\;; 0.5,16)\) and \(\mathcal L_2 = (1,6)\).

Todo

Exercise A: What is the expected return of each lottery?

Todo

Exercise B If the consumer has vNM preferences (expected utility), which lottery does he prefer?

Todo

Exercise C: Does the utility function \(u(Z) = Z\) give the same choice?

We can compute expected utility for a utility function:

for a general lottery with \(S\) states, \(\mathcal L = (p_1,Z_1;...,;p_S,Z_S)\) using a few Python tricks:

def u(z,sigma):

return z**(1.0-sigma)/(1.0-sigma)

def eu(zs,ps,sigma):

return np.sum([p*u(z,sigma) for p,z in zip(ps,zs)])

ps = [0.5,0.5]

zs = [0.0,16.0]

eu(zs,ps,0.5)

What do you get when we call this function eu()?

In a situation with certainty, utility is ordinal: only the ordering matters. However, in a risky situation, utility \(u\) is cardinal, because the expected utility \(\mathbb{E}_{L} u\) depends linearly on probabilities. Hence, a monotone transformation (stricly increasing) of \(u\) does not preserve preferences. Only affine transformations of the form \(\widehat u = a u +b\) with \(a>0\) yield the same preferences.

\[\begin{split}\begin{aligned} \mathbb{E}_{L_1} \widehat u \geq \mathbb{E}_{L_2} \widehat u & \iff a\mathbb{E}_{L_1} u + b \geq a\mathbb{E}_{L_2} u + b \\ & \iff \mathbb{E}_{L_1} u \geq \mathbb{E}_{L_2} u\end{aligned}\end{split}\]

However, the expected utility \(\mathbb{E}_{L} u\) itself is ordinal, indeed:

\[\begin{aligned} \mathbb{E}_{L_1} u \geq \mathbb{E}_{L_2} u & \iff f(\mathbb{E}_{L_1} u) \geq f(\mathbb{E}_{L_2} u) \end{aligned}\]

for any function \(f\) which is strictly increasing.

Risk Aversion¶

Risk attitudes may vary from one person to the next:

Risk aversion: If \(L_0 = (p, X\;; 1-p,Y)\) and we denote the expected value \(E_{L_0}Z = p X + (1-p)Y\), then the consumer is averse to risk if he prefers \(L_1' = (1,E_{L_0}Z)\) to \(L_0\).

Risk Loving: He (she) prefers \(L_0 = (p, X\;; 1-p,Y)\) to \(L_1' =(1,E_{L_0}Z)\)

Risk Neutrality: The consumer is indifferent bewteen \(L_0 = (p, X\;; 1-p,Y)\) and \(L_1' =(1,E_{L_0}Z)\).

What do we observe? Lots of risk aversion, some risk neutrality, among richer individuals and a bit of risk loving.

Risk aversion and Concavity¶

Risk aversion

The consumer has a utility function \(u\). In a vNM context, our only degree of freedom to model risk attitudes is the utility function. Properties of \(u\) are therefore central.

Fix two states \((X,Y)\) and the probability \(p\) that \(X\) is realized. The expected payoff is \(E_{L}Z = pX + (1-p)Y\).

Risk aversion implies

\[u(E_{L}Z) > pu(X) + (1-p)u(Y).\]

A function \(u\) which fits this inequality needs to be concave (see the math tools). In statistics, this result is Jensen’s inequality which arises when the function is concave. The risk-loving case corresponds to a convex function.

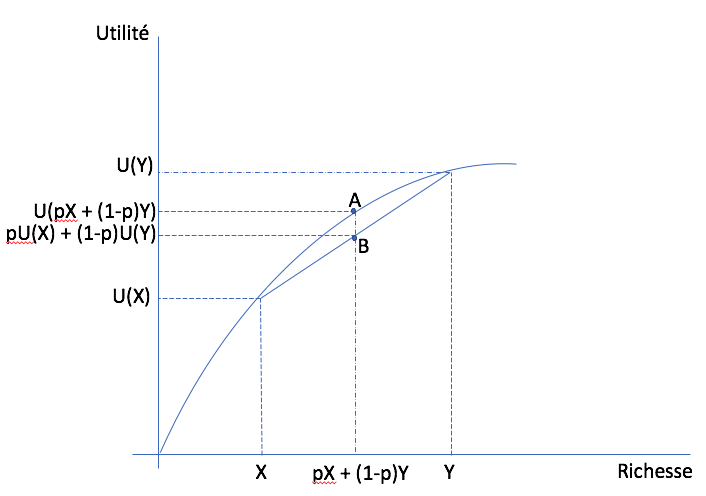

In the wealth-utility space, consider a lottery on \((X,Y)\) with probability \(p\) that \(X\) is realized. Starting on the horizontal axis, expected wealth is between \(X\) and \(Y\) since \(p\) is between zero and one. On the vertical axis, we can also do the same thing for expected utility, with the same \(p\). Varying \(p\), we get the straight line that attaches points \((X,Y)\) to the utility function. Since the function is concave, this line (or cord) is below the function itself. So utility evaluated at expected wealth (point A) is always above expected utility (point B). This holds for all \(p\).¶

Todo

Play around with this example from EconGraph.org.

Risk neutrality

If an individual is risk neutral, there is indifference between

\[\mathcal L = (p, X\;; 1-p,Y) \quad and \quad \mathcal L' = (1,E_{L} Z)\]

The utility function is therefore constrained to be linear in wealth \(u(Z) = a Z + b\), with the special case \(u(Z) = Z\).

Measuring Risk Aversion¶

How to measure risk aversion? How do we compare two individuals and say that one is more risk averse than the other? Two measures are useful for this purpose: the coefficient of absolute and relative risk aversion.

Absolute risk aversion coefficient:

\[A(Z) = -\frac{u''(Z)}{u'(Z)}\]

Relative risk aversion coefficient:

\[R(Z) = -\frac{u''(Z)Z}{u'(Z)}\]

Why these two measures? Since risk aversion si related to concavity, both measures increase when the second derivative increases (there is a negative sign in front since the second derivative is negative when function is concave). Then, we normalize by marginal utility \(u'(Z)\), to fix units since \(u\) is ordinal. Another way of thinking about it is that it is the percent change in the marginal utility.

The absolute measure allows to look at risk aversion for lotteries involving absolute payoffs. The relative coefficient allows to look at the degree of risk aversion for a lottery which is proportional to wealth.

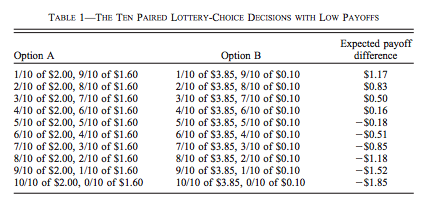

How do we measure this coefficient? One method is the multiple price list (MPL). Holt et Laury (2002) have used MPLs to measure risk attitudes.

A multiple price list presents two lotteries under different probabilities and payoff configuration. The respondent has to choose the lottery he prefers. There is often an incentive mechanism which rewards participants. Here is an example from Holt and Laury:

We could use a utility function of the form,

We can show that \(R(Z) = r\), and therefore this utility function is often referred too as CRRA (constant relative risk aversion).

Risk Premium¶

Consider the lottery \(L =(p,X\;;1-p,Y)\). Denote \(E_{L}Z\) expected wealth of the lottery \(E_{L}Z = pX+ (1-p)Y\). We could be interested in \(Z'\) such that

\(Z'\) is a certainty equivalent for \(L\) given preferences represented by \(u\).

If the agent is risk averse, \(Z' < E_{L}Z\) and we denote \(\pi = E_{L}Z-Z'\) the risk premium. Its interpretation depends on the context. When the action is to take on risk (by default the agent does not have risk), we interpret this as the minimal compensation to take on risk. It represents the minimal amount of money we need to give so he takes on risk. In a stock market investment decision, the excess return required by a risk averse investor is equal to the risk premium. The more risky is the investment, the more he will demand in terms of compensation.

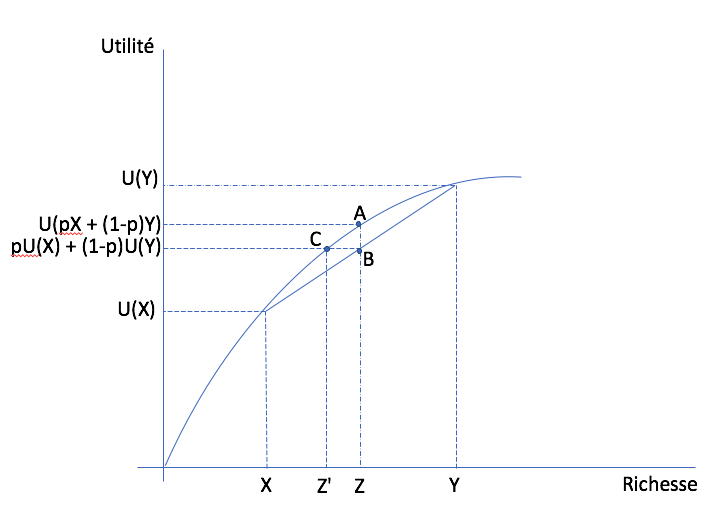

In the wealth-utility space, consider a lottery on \((X,Y)\) with probability \(p\) that \(X\) is realized. Point C gives the certainty equivalent wealth. Hence, certainty equivalent wealth is \(Z' < E_{L}Z\) and the risk premium is \(\pi = E_{L}Z-Z'\).¶

In insurance, the risk premium is equivalent to the maximum willingness to pay of the agent to eliminate the risk since the default (no insurance) is risky while full insurance eliminates the risk. It is therefore the maximum price the agent is willing to pay.

Todo

Exercise D: An agent has preferences represented by \(u(Z)=\log Z\). Her initial wealth is \(Z_0 = 100\) and she faces the risk of loosing 50 with probability 0.5 and win 50 with probability 0.5. What is the maximum price she is willing to pay for an insurance that eliminates the risk?

An approximation to the risk premium exists for small risks. Denoting \(\sigma^2\) the variance of a small risk with mean zero, the risk premium for an agent with initial wealth \(Z_0\) is well approximated by:

The risk premium increases with risk aversion and with the variance of the risk.

Todo

Exercise E: With \(u(Z) = \sqrt Z\), is the risk premium smaller than in the previous exercise?

Todo

Play around with this example from EconGraph.org.

As we show in the notebook below, we can find the risk premium numerically for any utility function and lotteries using bisection in Python.

Insurance¶

The insurance market exists in part because the population is generally risk averse. There exists insurance for pretty much every risk you can think of. Even our governments set up what is called social insurance program to help individuals when they face hardship (think of the Employment insurance system in Canada).

Take unemployment. Consider a simple example with two workers who can be in the following states:

Employed with probability 0.5, income of 100

Unemployed with probability 0.5, income of 0

Denote realized incomes of the two workers \(I_i\) (\(i=1,2\)). An employment insurance scheme may mandate that both receive \((I_1+I_2)/2\) no matter their employment status.

Insurance is beneficial ex ante (before the risk gets realized) for the two agents if they are risk averse:

Without insurance: expected utility of each is \(.5 [u(0) + u(100)]\)

With insurance, there is a 25 % probability that both get 0, 50% that one works, 25% that they both work. Hence, expected utility of each agent is \(.25[u(0) + 2u(50) + u(100)]\).

According to vNM preferences, insurance is beneficial if

\[.25[u(0) + 2u(50) + u(100)] > .5 [u(0) + u(100)]\]

or if \(u(50) > .5[u(0)+u(100)]\). Hence, we need the utility function \(u\) to be concave or the agent to be risk averse (again Jensen’s inequality).

In practice, employment insurance could be informal. But enforcing payments after risks are realized may be costly. The worker who did not lose his job may not want to share with the other. Hence, employment insurance schemes lower these costs by enforcing the payment of premiums and benefits. The same goes for other insurance markets.

The other advantage of having an insurer is that the benefit to consumers of insurance grows with the number of insured individuals. For this, we need to invoke the law of large numbers.

See also

Read this discussion of how to improve employment insurance.

Law of Large Numbers

Consider a random variable \(Z\) equal to \(X\) with probability \(p\) and \(Y\) with probability \(1-p\)

If \(Z_1, \cdots , Z_n\) are independent with the same distribution \((p,X \;; 1-p,Y)\) then

\[si\; N \to +\infty,\quad \frac{1}{N} (Z_1 + Z_2 + \cdots + Z_n) \to pX + (1-p)Y\]The average of realizations, which is still random when \(N\) is small, becomes almost certain when N tends to infinity.

Mutualization

When a large number share the risk, risk is eliminated trough mutualization. The insured receive exactly the average.

If agents are risk averse, this result is admirable.

Insurers need to issue debt to finance their operation. This debt, often in the form of corporate bonds, needs to reward investors for the risk inherent to each insurer. Insurers who are riskier, perhaps because their portfolio is less diversified (smaller), will need to pay a premium on their debt. This in turn may translate into higher premiums.

Insurance and Entrepreneurship¶

Becoming entrepreneurs

An individual has wealth of 9 and may decide to keep this wealth or use it to start a business. His final wealth, if he starts a business can be represented as a lottery: \(L = (.5,0 \;; .5,25)\). His vNM preferences are represented by \(u(Z) = \sqrt{Z}\).

Todo

Exercise F: Does he start the business?

Angel Investors

Instead of investing alone, the entrepreneur may obtain some seed money from an angel investor. Suppose he gives half the capital for half the profits from the business.

The entrepreneur keeps 4.5 with certainty if he starts the business (the other half is given by the angel investor). In exchange he gives up a bit of profit if things go well.

The lottery is now :math:` L’ = (.5,4.5 ;; .5,17)`

Todo

Exercise G: What will be his choice?

The TV show, Les Dragons (Dragon’s Den) from Radio-Canada and CBC provides a direct illustration of what is happening. Participation from one of the Dragon is always conditional to a share of the profits. Negociation takes place on the share of profits that the entrepreneur needs to give up in order to obtain an investment from the dragon. Here is an example (in french) of two entrepreneurs who drove a hard bargain…

Risk Sharing in Action¶

Watch this podcast with Henri-Paul Rousseau, adjunct Professor at HEC Montreal, and CEO of several financial institutions over his long career.

Critics of Expected Utility¶

Consider the following experiments.

Choice Experiment I

Draw an integer number between 0 and 99 with probability 1/100 for each integer:

Lotteries |

0 |

1-10 |

11-99 |

\(L_1\) |

50 |

50 |

50 |

\(L_2\) |

0 |

250 |

50 |

Choice Experiment II

Now, consider another pair of lotteries with the same rules for picking a number.

Lotteries |

0 |

1-10 |

11-99 |

\(L_3\) |

50 |

50 |

0 |

\(L_4\) |

0 |

250 |

0 |

Maurice Allais and his Paradox

Todo

Exercice H: Show that \(L_1 \succ L_2\) and \(L_4 \succ L_3\) are not consistent with expected utility.

Read the story behind the paradox. Munier (1991)

Choice Experiment III

An urn consists of 90 balls. 30 are red. The other 60 are either black or white. The proportion of white and black balls is not know. We ask you to make a choice between these lotteries:

Loteries |

red |

black |

white |

\(L_1\) |

50 |

0 |

0 |

\(L_2\) |

0 |

50 |

0 |

Choice Experiment IV

Do the same in this context.

Loteries |

red |

black |

white |

\(L_3\) |

50 |

0 |

50 |

\(L_4\) |

0 |

50 |

50 |

Ellsberg Paradox

Todo

Exercise I Show that the combination of choices \(L_1 \succ L_2\) and \(L_4 \succ L_3\) is inconsistent with expected utility for any beliefs about the proportion of white or black balls.

Daniel Ellsberg is well known for this paradox, but perhaps much more for his battles with the American government. Pentagon Papers

Kahneman and Tversky: Perspectives

The authors, both recipients of a Nobel, show that we are influenced by perspectives (often named framing) when we make choices, in particular when risk is involved:

Imagine a new virus could kill 600 individuals. Two interventions are shown:

(Positive perspective): A) 200 are saved, B) 1/3 probability that 600 are saved, 2/3 no one is saved.

(Negative perspective): C) 400 will die, D) 1/3 probability no one dies, 2/3 probability they all die.

In practice, A is more popular than B, but D is more popular than C. In terms of lives saved, A is the same lottery as C and B as D.

If these framing effects are of interest, you are encouraged to read: Khaneman and Tversky (1979)

Python Risk Example¶

![]()